Microsoft’s fourth quarter earnings preview: Progress momentum deserves consideration

When will Microsoft report earnings?

Microsoft is scheduled to launch its fourth quarter (This autumn) monetary efficiency after the U.S. inventory market closes on Tuesday, July 30, 2024.

Microsoft Earnings—What to Count on

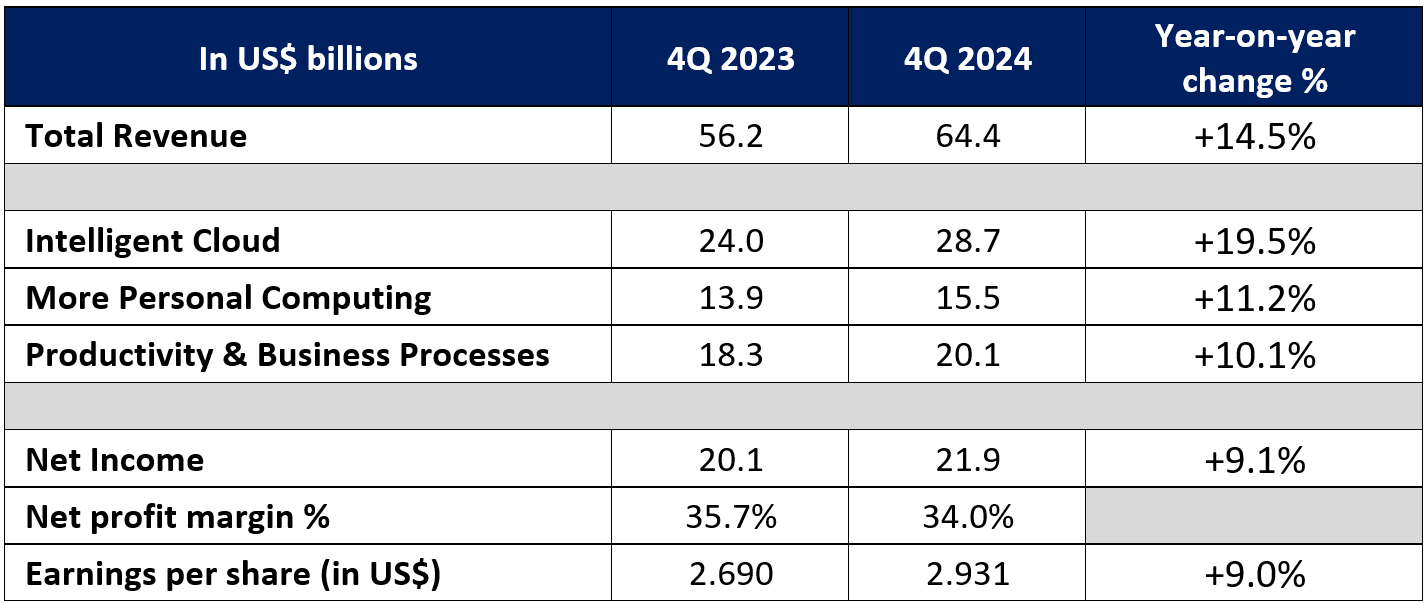

The market expects Microsoft’s income within the upcoming fourth quarter of 2024 to extend by 14.5% year-on-year to US$64.4 billion, greater than US$56.2 billion within the fourth quarter of 2023. 17.0% slowed.

Earnings per share (EPS) are anticipated to develop 9% year-over-year to $2.931, up from $2.69 within the fourth quarter of 2023.

Cloud enterprise stays in focus to drive worthwhile progress

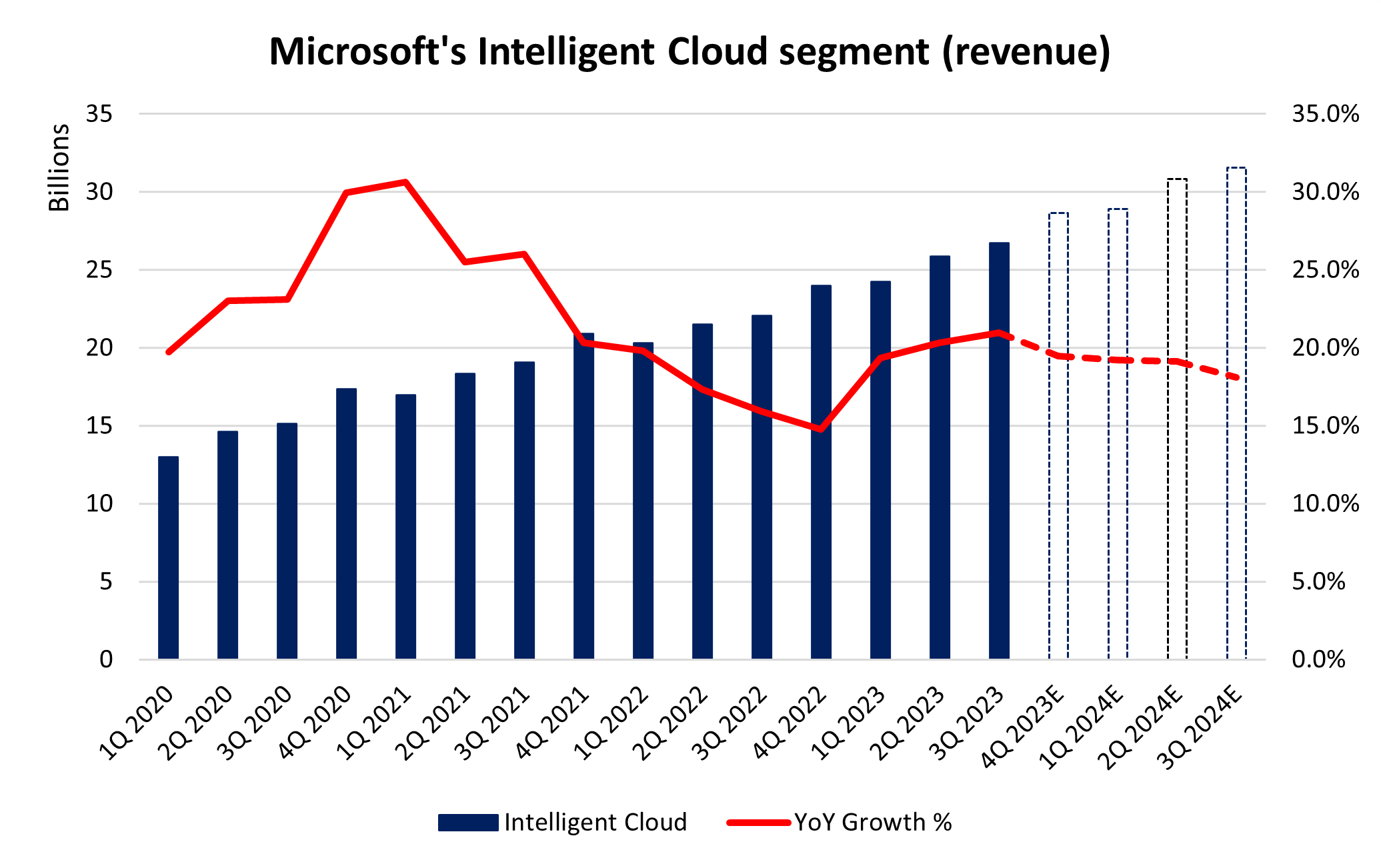

Microsoft’s sensible cloud enterprise stays Microsoft’s quickest rising division, accounting for 43% of its whole income. Within the fourth quarter of 2024, the phase is anticipated to develop 19.5% yearly to achieve $28.7 billion.

Beforehand, stronger-than-expected progress on this phase was one of many key causes for Microsoft’s inventory value surge. This quarter, Microsoft’s market share within the world cloud infrastructure market efficiently elevated to a file excessive of 25%, trailing solely Amazon AWS’s 31%.

There’s little room for error going ahead, given a sequence of feedback from Microsoft’s administration workforce that additionally appeared to set the stage for expectations that sturdy adoption of Azure AI providers will proceed.

Administration has beforehand emphasised that the variety of Azure AI clients continues to develop, common spending continues to extend, and “income progress from migration to Azure accelerates.” Extra famously, Chief Monetary Officer Amy Hood mentioned on the time that “near-term AI demand is barely greater than accessible capability.”

Supply: Refinitiv

Beforehand, product differentiators got here into play throughout the board. The expansion momentum deserves consideration.

The continued progress of quite a lot of merchandise stays worthy of consideration. Azure Arc, which permits clients to execute Azure providers wherever (throughout on-premises and multi-cloud platforms), tripled the variety of clients final quarter to 33,000.

New synthetic intelligence capabilities have pushed LinkedIn’s premium progress, with income rising 29% year-on-year. Pushed by the surge in GitHub Copilot adoption, GitHub’s income additionally elevated by greater than 45% in contrast with the identical interval final yr. Microsoft Cloth is its next-generation analytics platform with greater than 11,000 paying clients. Copilot in Home windows can also be accessible on practically 225 million Home windows 10 and Home windows 11 computer systems, triple the quantity from the earlier quarter.

Mass adoption of those options is more likely to proceed, and buyers shall be holding an in depth eye on future progress progress.

Cloud and synthetic intelligence infrastructure funding value strain turns into focus

Microsoft mentioned final quarter that it anticipated capital expenditures to extend “considerably quarter-over-quarter” on account of elevated funding in cloud and synthetic intelligence infrastructure. Nevertheless, the market is happy with the corporate’s steering, with working margins anticipated to extend by greater than 2 share factors year-over-year in fiscal 2024 regardless of important investments, whereas working margins will solely decline roughly 1 share level year-over-year in fiscal 2025 .

Any resilience within the firm’s margins can be encouraging. Market individuals additionally wish to make sure that big funding value expenditures might be shortly expanded into profit-making capabilities reasonably than long-term measures. Folks might recall that Meta’s inventory value plummeted 19% in its earlier earnings launch as buyers didn’t consider within the firm’s “long-term” investments in synthetic intelligence and the Metaverse.

Different key areas might stabilize at double-digit progress

Microsoft’s “private computing” enterprise noticed shocking progress within the third quarter of 2024, pushed by better-than-expected efficiency from gaming and Home windows OEMs. The annual progress price might stabilize at 11.2% within the fourth quarter of 2024, and the restoration is anticipated to proceed to keep up low double-digit progress.

Likewise, the “productiveness and enterprise course of” phase is more likely to submit stable 10% year-over-year progress in This autumn 2024, additional pushed by common income per consumer (ARPU) progress from continued E5 momentum and early Copilot progress on Microsoft 365 of help.

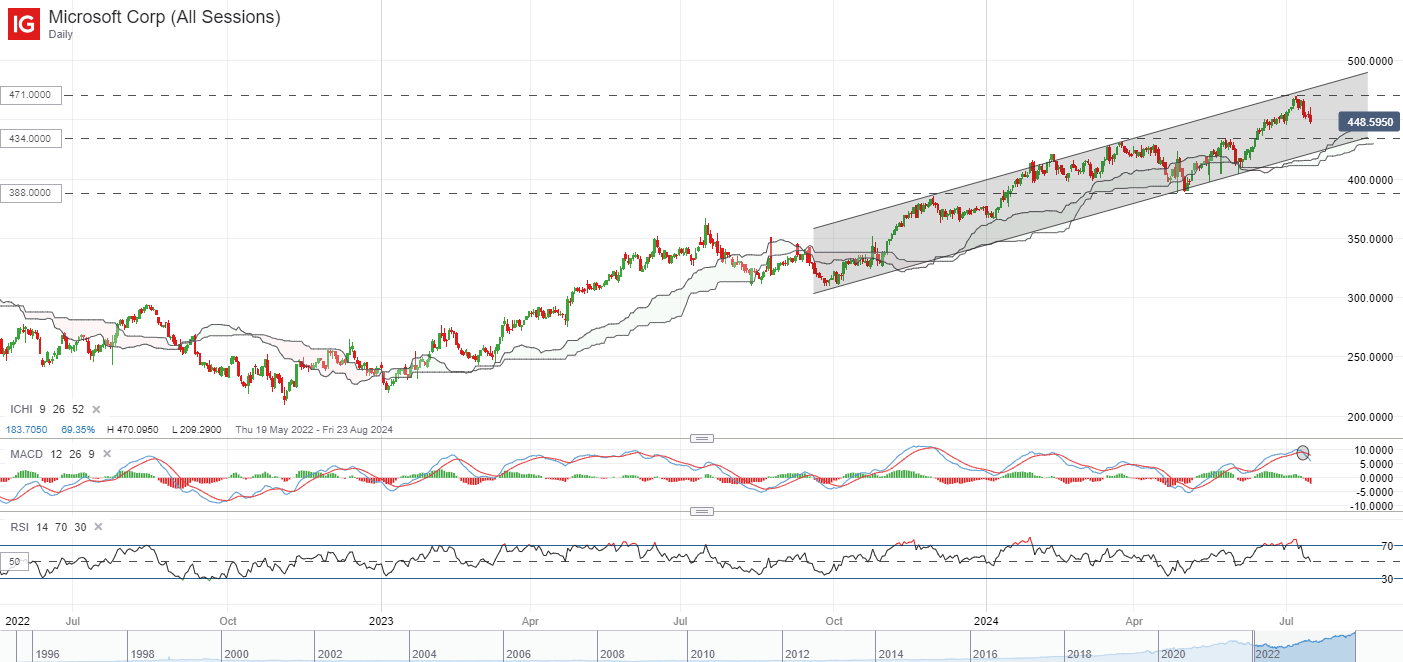

Technical Evaluation-Microsoft inventory value is on an upward pattern

From a technical perspective, Microsoft inventory has been in an uptrend since October 2023, exhibiting greater highs and better lows. The $471.00 stage finds some near-term resistance. There may be additionally a bearish crossover on the day by day Shifting Common Convergence/Divergence (MACD), which can improve the probability of a respite within the close to time period.

Any deeper retracement might make the $434.00 stage a key help stage to carry. That mentioned, it could take extra time to sign a broader pattern change, probably with a collapse of the ascending channel as the primary signal. Till then, the broader uptrend will prevail and speedy resistance at $471.00 will should be overcome.

Supply: IG Charts